It's August. The fiscal year still has four months to run. But somewhere in the back of your mind, you already know what's coming: budget season. The spreadsheets you'll inherit from last year. The vendor contracts you'll need to review. The conversation with the full board about whether to raise assessments — and by how much. The homeowners who will argue it's too much, and the ones who will quietly worry it's not enough.

For most HOA treasurers, budget season is the most dreaded stretch of the year. It's time-consuming, politically charged, and built almost entirely on assumptions that may or may not hold. Work too fast and you end up approving a budget you'll be managing around for the next 12 months. Start too late and you're scrambling to get documents out the door before the fiscal year flips.

The good news is that HOA budgeting doesn't have to be this hard. The boards that handle it most smoothly share a common trait: they have a process, and they start it early enough to follow it properly. In this guide, we'll walk through that process step by step — from the moment you pull last year's actuals to the moment the board votes to approve the new budget.

Step 1: Start Earlier Than You Think You Need To

The single most common mistake HOA treasurers make is starting the budget process too late. For communities with a January 1 fiscal year, budget approval typically needs to happen in November — and in many states, homeowners must receive notice of the proposed budget and any assessment changes 30 to 60 days before approval. That means first drafts need to be ready by early October at the latest.

Working backward from those deadlines, serious budget work should begin in August or September. That's not arbitrary — it's what the timeline actually requires if you want to gather vendor quotes, review reserve fund projections, validate last year's actuals, and give board members enough time to review the draft before the approval meeting.

In practice, most boards don't kick off the process until October or November. The result is a rushed budget built on incomplete information, approved under time pressure, with assumptions nobody had time to challenge. Then those assumptions start failing in February, and the treasurer spends the rest of the year explaining variances that were baked in from the start.

The rule of thumb: If your fiscal year begins January 1, your budget kickoff meeting should happen no later than September 15. For other fiscal year start dates, count back four to five months. Starting early is the single highest-leverage thing a treasurer can do for budget quality.

Step 2: Understand That You're Building Two Budgets

This is where many HOA budget processes go structurally wrong, and it's worth understanding clearly before you write a single number.

An HOA annual budget is actually two distinct financial plans sitting side by side: the operating budget and the reserve contribution budget. These two components have completely different purposes, different time horizons, and different methodologies. Treating them as interchangeable line items in the same spreadsheet — which is common — leads to decisions that look reasonable in isolation and cause problems in practice.

The operating budget is about the coming 12 months. It covers day-to-day expenses: landscaping, insurance, utilities, management fees, routine maintenance, administrative costs. These are the predictable, recurring costs of keeping the community running. The goal is to match assessment income to operating expenses, building in a reasonable contingency margin.

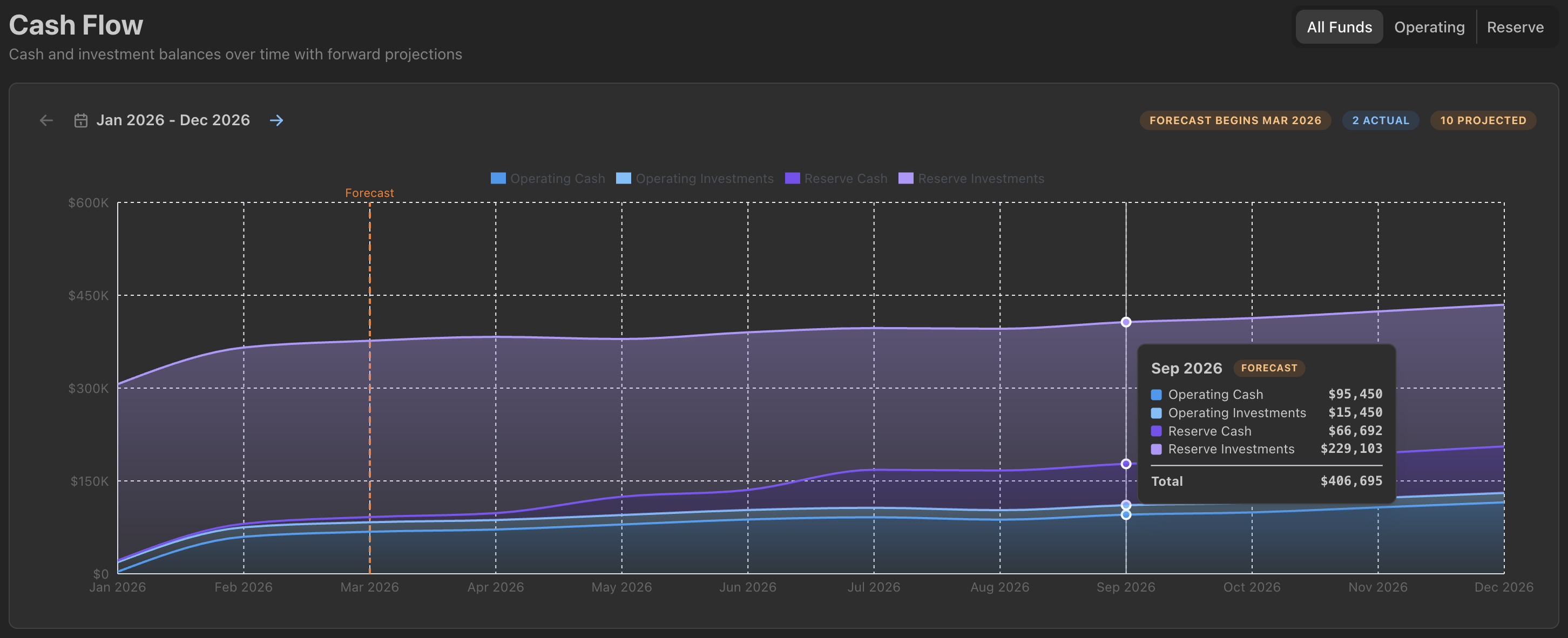

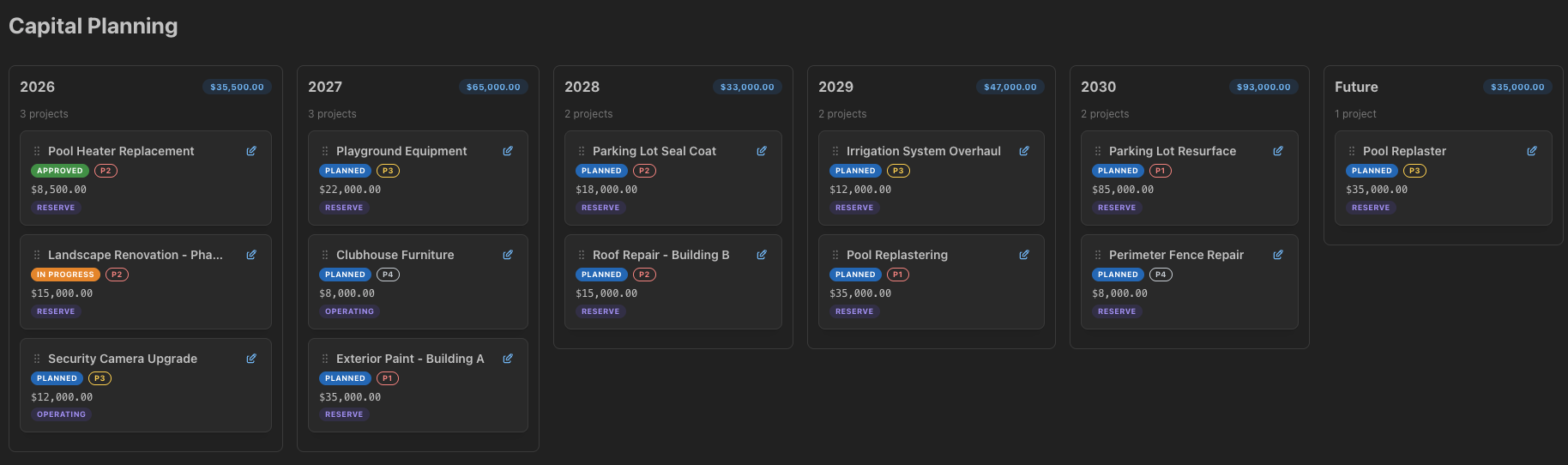

The reserve contribution budget is about the next 5 to 20 years. It's the monthly amount the community needs to be setting aside now to fund future capital replacements — the roof that needs replacing in eight years, the parking lot in six, the elevators in twelve. Reserve contributions aren't expenses; they're investments in the community's future financial health.

"Every year we'd figure out the operating budget first and then see what was left for reserves. The reserve number was basically what we could afford after everything else was covered. It took a new treasurer to point out that we had it exactly backwards — and that's why our reserve fund was underfunded."

This is a surprisingly common pattern. Reserve contributions should be determined by what the reserve fund actually needs — based on a current capital project schedule and a target funding level — not by what's left over after operating expenses are tallied. If the reserve requirement means assessments need to increase, that's important information the board needs to act on. Burying it under operating line items obscures the problem rather than solving it.