At the October board meeting, everything looked fine. The treasurer pulled up the bank portal, confirmed the operating account had $112,000, and reported that the community was "in great shape financially." Nobody asked any follow-up questions. Nobody needed to.

By December, the Maplewood Crossing HOA couldn't pay their landscaping contractor on time. Their $112,000 balance had obscured something the spreadsheet never showed: three large annual insurance premiums, a roof repair deposit, and Q4 assessment refunds were all due within the same six-week window. They had the money—they just didn't have it at the right time.

This is the most common and most misunderstood financial problem in HOA management. It isn't about saving enough or spending too much. It's about cash flow: the timing of money coming in and going out. Most HOA boards never see the problem coming—because they're looking at the wrong number.

The Balance Trap: Why Your Bank Account Is Lying to You

Ask any HOA treasurer how the community is doing financially, and the first thing they'll reach for is the current account balance. It's human nature—the number is right there, easy to read, intuitively satisfying. If it's high, things are good. If it's low, things are worrying.

The problem is that a balance is a snapshot taken at one instant in time. It tells you where you've been, not where you're going. It says nothing about what's owed in the next 30 days, whether a large payment is already in transit, or whether assessment income is about to slow down because a homeowner entered a payment plan.

"We had more money in the bank in October than we'd had in years. Three months later we were asking our property manager if we could delay their invoice." — HOA Board President, Scottsdale, AZ

The balance trap ensnares even experienced boards because the consequences are delayed. A cash flow problem in October might not surface until January. By then, the board has long since moved on from the October meeting, and nobody connects the dots.

Mistake #1: Treating All Cash as Available Cash

Many HOAs maintain one or two bank accounts and view the combined balance as money that's available to spend. In practice, a meaningful portion of that balance is already committed: it's been budgeted for specific line items, it represents prepaid assessments that belong to future quarters, or it's informally earmarked for a project the board discussed three meetings ago.

When treasurers don't track committed funds separately from truly available cash, they make decisions based on a fictional number. A board approves a $15,000 parking lot patch because the account shows $90,000. What they didn't account for: $20,000 in landscaping invoices not yet received, a $25,000 roofing contractor deposit due in 45 days, and $18,000 in reserve contributions that need to be swept this month.

The math looks fine until it doesn't. And it tends to stop looking fine right around the time a vendor calls asking where their check is.

Mistake #2: Ignoring Seasonal Cash Flow Patterns

HOA cash flow is rarely steady. Assessments often come in quarterly or semi-annually, creating predictable valleys between collection periods. Maintenance expenses tend to cluster: landscaping contracts ramp up in spring, HVAC servicing happens in the fall, and year-end often brings insurance renewals, audit fees, and property management contract payments all at once.

Most HOA boards know, in a general sense, that some months are tighter than others. What they rarely do is map it out explicitly. That's where the trouble starts.

Consider a typical 150-home community with quarterly assessments. In the month after assessments are due, the operating account looks robust. Eight weeks later, before the next assessment cycle, it looks thin. A board reviewing the financials in that thin window might panic unnecessarily. A board reviewing during the flush window might approve discretionary spending that creates a problem they won't see until next quarter.

"We learned the hard way that October feels rich and February feels poor—and neither number tells you much about our actual financial health." — HOA Treasurer, Denver, CO

Mapping your seasonal pattern requires only a few hours of historical data analysis, but the insight it produces is worth far more. Once you know your cash flow rhythm, you can time major payments, schedule reserve contributions, and have an honest conversation at every board meeting about where you are in the cycle.

Mistake #3: Confusing Operating Cash Flow With Reserve Health

Operating cash flow and reserve fund health are two separate things that affect each other but should never be confused with each other. Healthy operating cash flow means the community can pay its day-to-day bills without stress. A healthy reserve fund means the community can pay for major capital repairs without levying a special assessment.

The mistake boards make is treating them as interchangeable. Some communities routinely borrow from reserves to cover operating shortfalls, intending to pay it back later—and then don't. Others stop funding reserves at the required percentage because "the operating account looks fine," not realizing they're trading future stability for present comfort.

The healthiest HOA boards treat reserve contributions as fixed obligations, exactly like an insurance premium or property management fee. Operating cash flow planning happens around that number, not at the expense of it. It requires more discipline in the short term, but it's the difference between a community that handles capital repairs smoothly and one that dreads every aging roof and crumbling driveway.

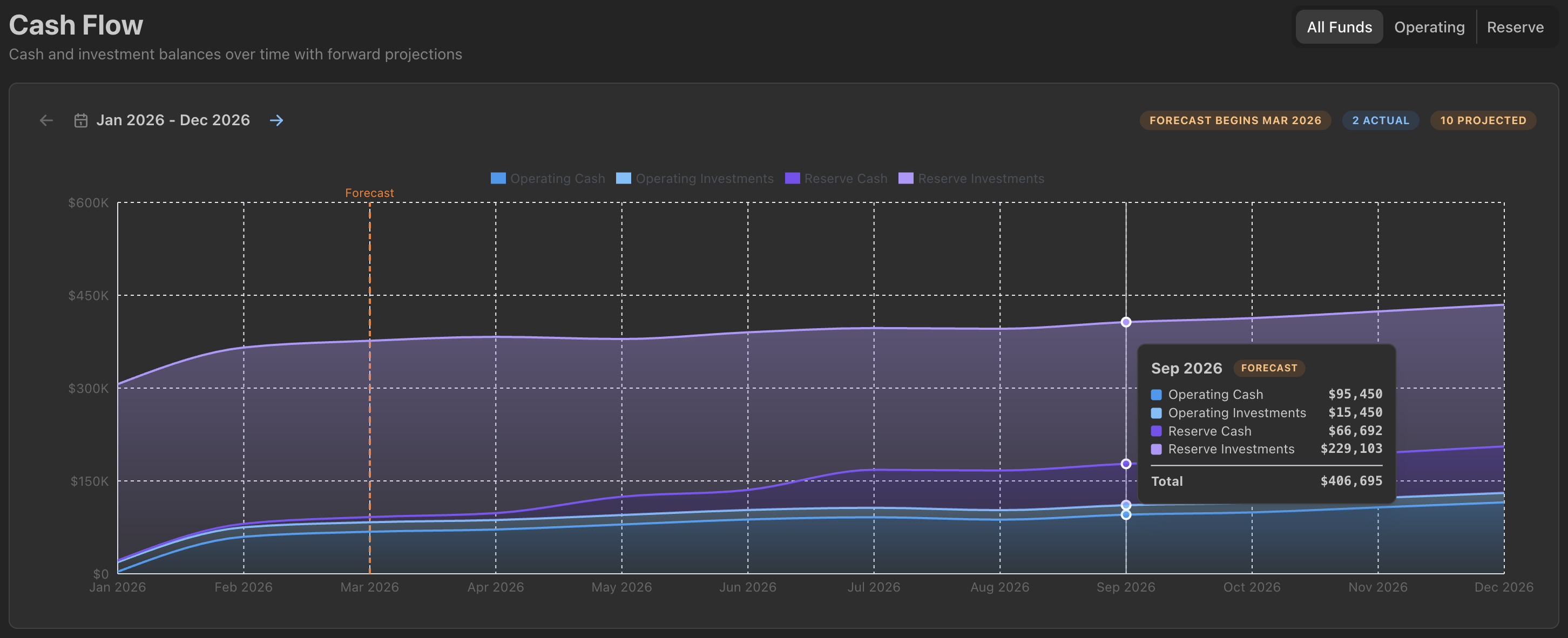

Mistake #4: No Forward-Looking Cash Flow Forecast

The most consequential cash flow mistake is also the simplest to describe: most HOA boards have no forward-looking projection at all. They review what happened last month, confirm the current balance, and adjourn. There's no model showing what the account will look like in 30, 60, or 90 days given known income and expenses.

This isn't laziness—it's a tool problem. Building a rolling cash flow forecast in a spreadsheet is genuinely tedious. You need to pull in assessment schedules, map out expected invoices, account for seasonal patterns, and update everything every month. Most volunteer treasurers don't have the time, even if they have the skill.

The result is a board that's perpetually surprised. Tight months feel like emergencies. Flush months feel like windfalls. Neither feeling is accurate—both reflect a lack of visibility into what's actually coming.

Tom Rivera had served as treasurer of a 200-unit community in Austin for three years before he built his first proper cash flow forecast. "I'd always known, roughly, when money was tight. But I'd never actually mapped it out. When I finally did, I saw that we'd been within $8,000 of not being able to cover payroll twice in the last two years. Nobody knew. I didn't know."