Picture this: It's 48 hours before your HOA's quarterly board meeting. Your treasurer has just discovered that the reserve fund balance is off from where the spreadsheet said it should be. Two homeowners went delinquent two months ago — but nobody noticed until now because the tracking was buried four tabs deep. And someone just forwarded an email from a vendor asking why the landscaping invoice hasn't been paid, because the budget line ran out in September.

Welcome to the reality of manual HOA financial management.

The hard truth is that most HOA boards don't know what they don't know. Not because they're careless — quite the opposite. It's because the tools most boards use were never designed to surface problems proactively. Spreadsheets don't send alerts. Static reports don't forecast. Manual processes create lag between when a problem starts and when someone finally sees it.

The result? Financial blind spots that quietly cost communities tens of thousands of dollars — often before anyone realizes there's a problem at all.

Here are the five most common financial blind spots affecting HOA boards today, and how our AI-enabled management platform is eliminating them before they become crises.

Blind Spot #1: Cash Flow Amnesia

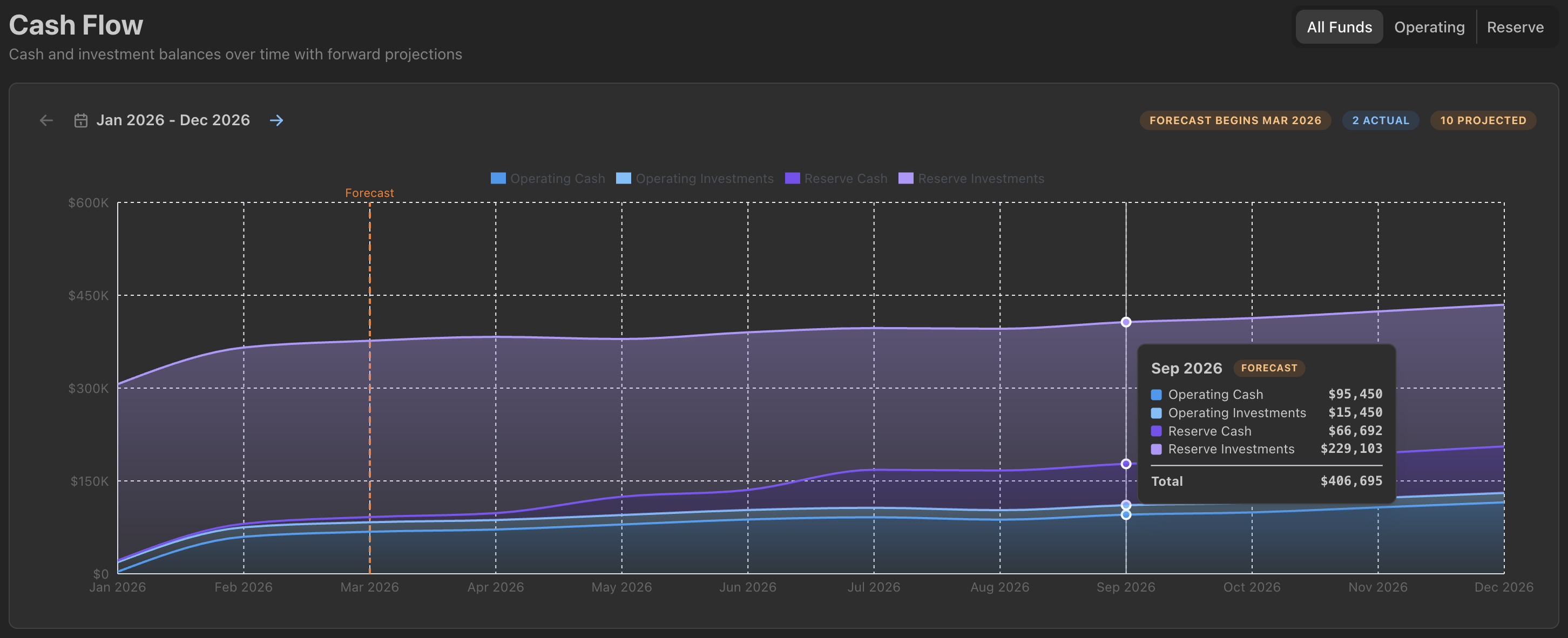

Most treasurers know their current bank balance. Very few can accurately answer: "What will our balance be in 90 days?"

This distinction matters enormously. A $150,000 balance today can look perfectly healthy — right up until you remember that $80,000 in landscaping contracts comes due next month, $35,000 in insurance renewal hits in 60 days, and the quarterly reserve contribution is $25,000. Suddenly, that healthy-looking balance is a cash crisis in slow motion, and nobody has sounded the alarm because the spreadsheet only shows what's already happened.

Traditional financial tracking is backward-looking by nature. It tells you where you've been, not where you're going. AI-powered cash flow forecasting changes this entirely, modeling your projected balance 12 or more months into the future — based on known expense patterns, assessment income timing, seasonal spending cycles, and scheduled capital projects.

What HOA LedgerIQ finds: Cash crunches before they happen, giving boards time to adjust project timing, optimize investment placement, or accelerate assessment collection — instead of scrambling when the account runs dry.

Blind Spot #2: Reserve Fund False Confidence

"We have reserves" and "we have enough reserves" are very different statements. On a spreadsheet, they can look identical.

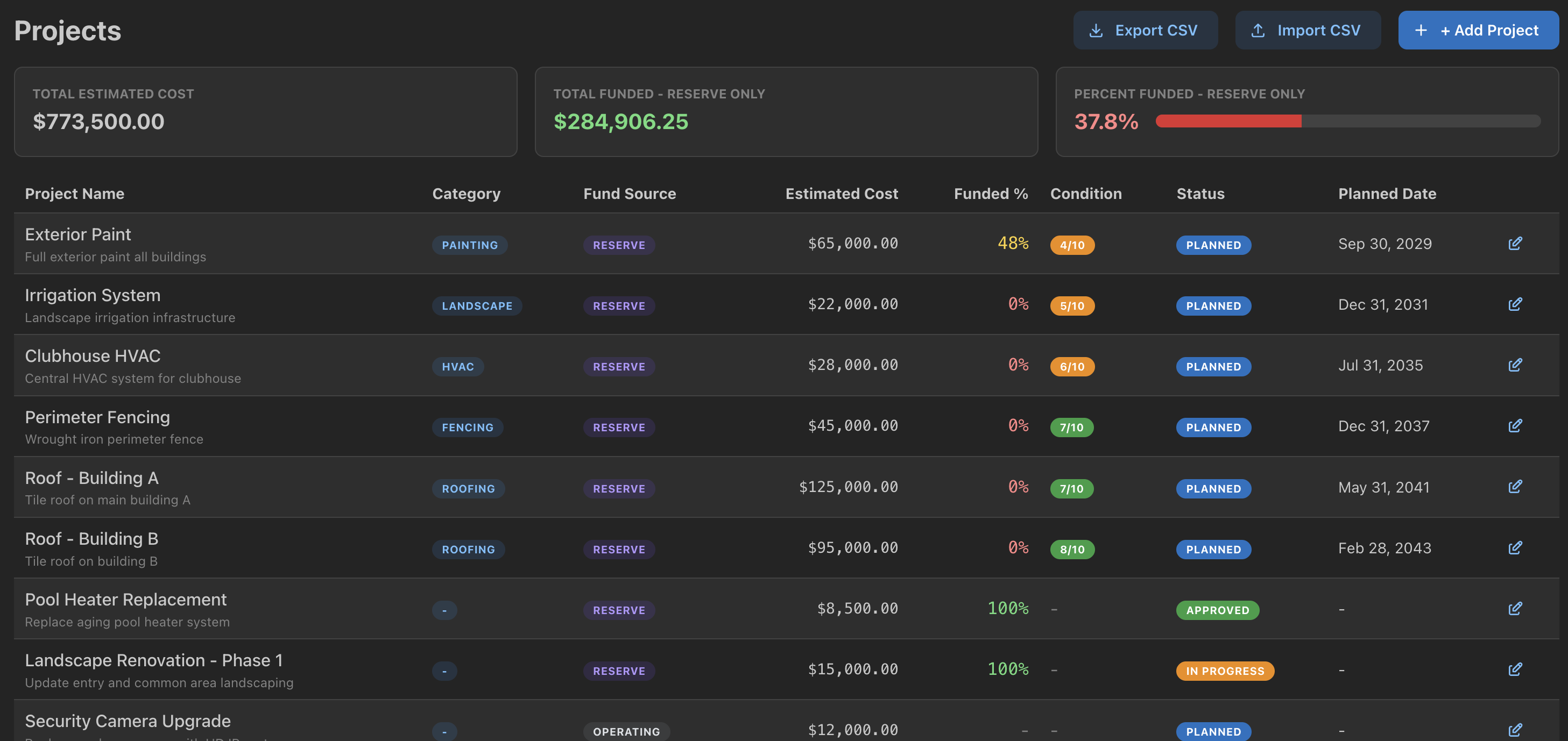

This is one of the most dangerous blind spots in HOA finance. A community might have $500,000 in their reserve account and feel financially secure. But without modeling that balance against the actual schedule of upcoming capital needs — roof replacement, HVAC systems, parking lot resurfacing, elevator modernization, pool equipment — it's impossible to know whether $500,000 is a cushion or a shortfall in disguise.

Reserve studies are supposed to solve this, but they have a critical structural flaw: they're static. The moment a reserve study is published, it begins going out of date. Actual spending differs from projections. Interest rates shift. Material costs change. Project timelines slip. A study completed in 2022 may be meaningfully misleading by 2026.

HOA LedgerIQ reserve tracking makes this a living, continuous process. It compares actual reserve fund contributions and balances against the schedule of upcoming capital needs in real time, generating a health score that updates as conditions change — not just when someone remembers to update the spreadsheet.

What HOA LedgerIQ finds: Reserve shortfalls 12 to 24 months before they become emergencies, giving boards time for corrective action — an adjusted contribution rate, a modest assessment increase — rather than a surprise special assessment that leaves homeowners furious and the board scrambling.

Blind Spot #3: Investment Income Left on the Table

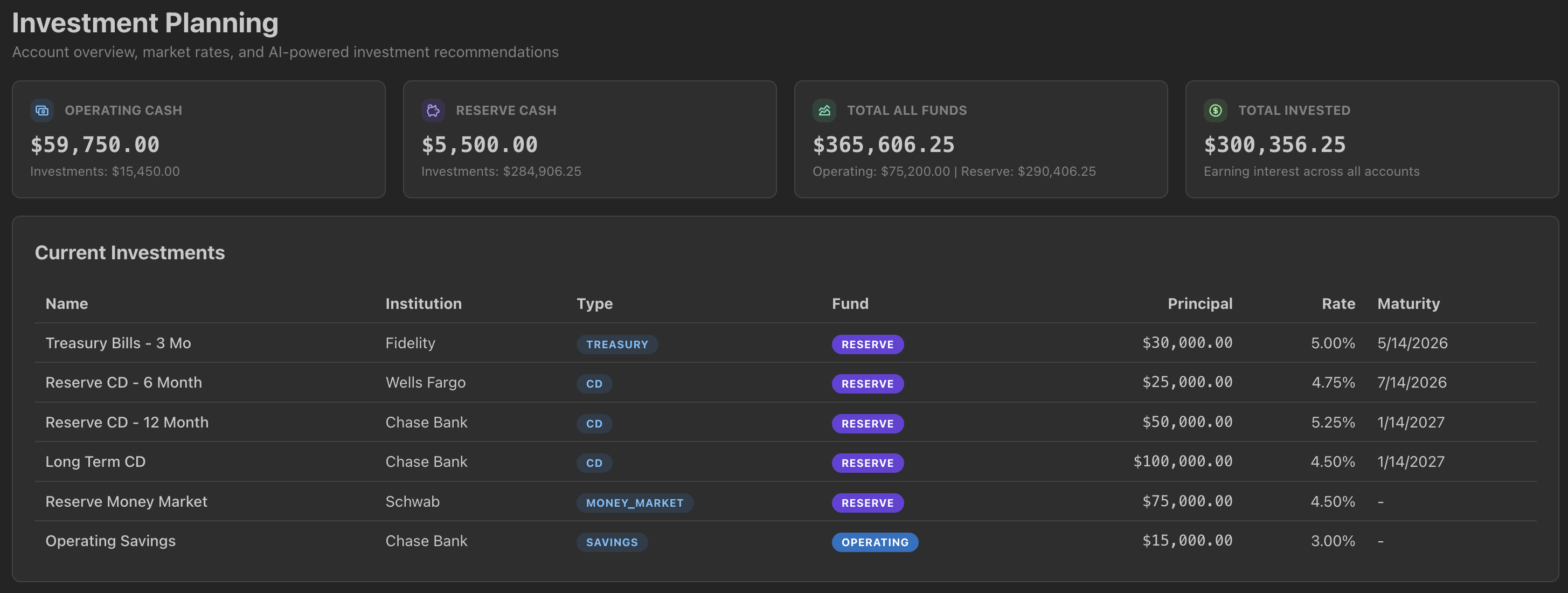

Here's a question worth asking right now: how much of your community's operating cash is sitting in a non-interest-bearing account?

For many HOAs, the answer is: most of it. Operating funds that aren't needed for immediate expenses tend to sit idle in basic checking accounts, earning nothing — while even modest deployment into high-yield savings, money market funds, or short-term CDs could be generating meaningful income for the community.

The hesitation is understandable. Deploying operating funds into any investment requires confidence that those funds won't be needed for expenses in the near term. Without reliable forward-looking cash flow projections, most treasurers keep everything liquid as a precaution — even when a meaningful portion could safely be put to work.

HOA LedgerIQ changes this calculus. By modeling projected cash needs against current balances, it can identify windows where idle funds can be safely deployed — and recommend specific strategies based on the timing and amount: a 30-day CD here, a 90-day treasury there, a sweep into a money market account while the next assessment cycle loads up.

What HOA LedgerIQ finds: Opportunities to earn additional investment income on idle funds — often thousands of dollars per year that most boards are simply leaving on the table without realizing it.