The meeting had been going for forty minutes and the board was deep into a debate about whether to replace the pool furniture this summer or push it to fall. Meanwhile, the treasurer's report had taken four minutes: she'd shown a bank balance, said everything looked "about where we expect it to be," and moved on.

Nobody asked a follow-up question. Nobody asked whether there was enough cash to cover the pool furniture if they approved it today. Nobody asked how the community's reserve contributions were tracking against the annual plan, or whether any large expenses were sitting in vendor inboxes waiting to be invoiced. The board wasn't being careless—they just didn't know what to ask.

That's the root problem in most HOA board meetings. The financial review happens, but it's a recitation of what already occurred rather than a forward-looking conversation about where the community stands and where it's heading. Five questions, asked consistently at every meeting, can completely transform that dynamic. They don't require financial expertise. They require only the discipline to stop and ask them every single time.

Question 1: What Does Our Cash Flow Look Like Through the End of the Quarter?

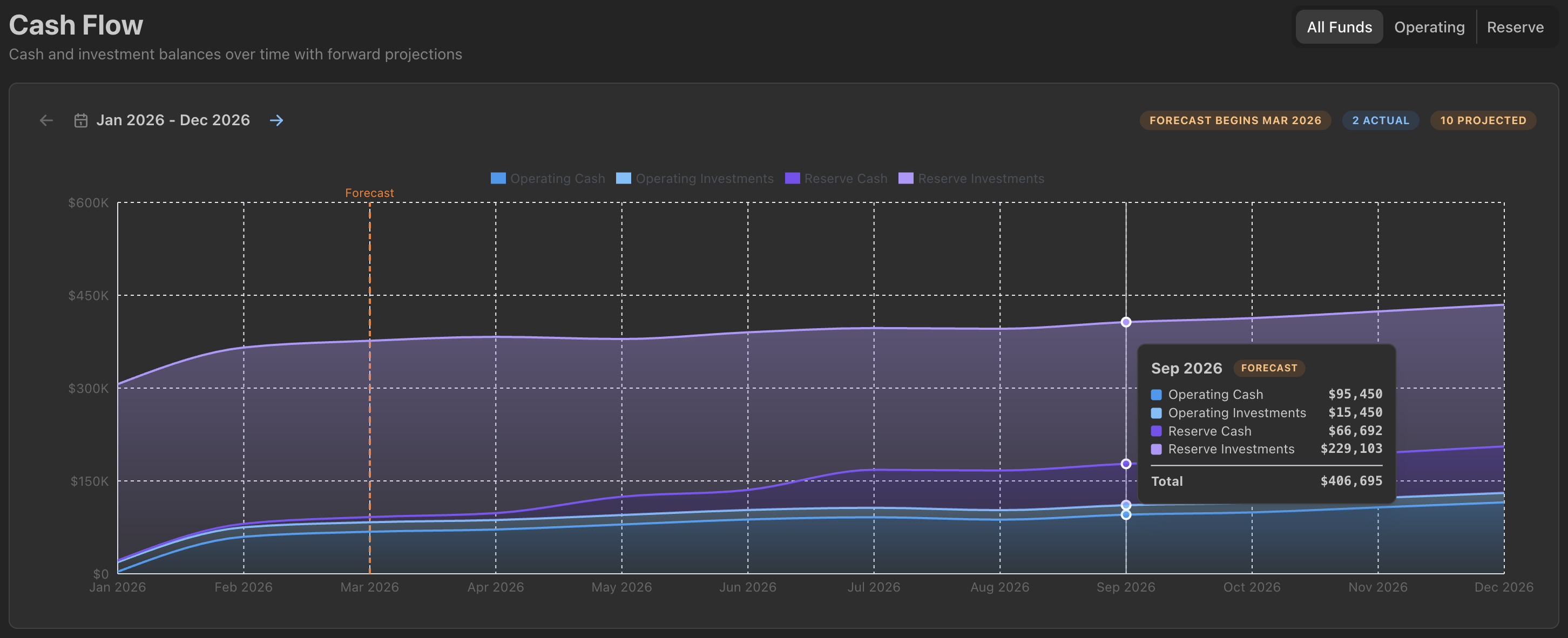

The most important financial question a board can ask isn't "what's in the bank?" It's "what will be in the bank in 60 to 90 days, given everything we know is coming in and going out?"

The distinction sounds subtle but it's enormous. A current bank balance tells you the result of decisions made weeks or months ago. A forward-looking cash flow projection tells you whether you have room to make decisions right now—or whether you need to slow down and conserve.

Consider a community with a $95,000 operating balance in October. On the surface, that looks healthy. But if $30,000 in annual insurance premiums are due in November, $22,000 in landscaping invoices are expected before year-end, and the next assessment cycle doesn't close until January, the real question isn't "do we have $95,000?"—it's "will we have $43,000 at the low point of Q4, and is that enough buffer?" Those are very different conversations.

"Every month I showed the board the bank balance. Then one November we couldn't pay our property manager on time and everyone acted shocked. The balance had never been higher in October. I finally understood that the balance isn't the answer—it's barely even the question." — HOA Treasurer, Mesa, AZ

Asking for a 90-day cash flow projection at every meeting takes the board out of the rearview mirror and puts them in the windshield. Over time, it becomes the most natural question in the room—and the one that prevents the most problems.

Question 2: Are We on Track With Reserve Contributions?

Reserve contributions are the HOA equivalent of a mortgage payment. Miss a few and the math catches up with you in ways that are far more painful than the short-term relief was worth. Yet many boards allow reserve contributions to slip—delayed by one month, reduced during a tight quarter, or simply forgotten in the noise of operating decisions—without ever explicitly discussing the trade-off they're making.

The question "are we on track with reserve contributions?" forces that conversation into the open. It's not accusatory—sometimes boards make a deliberate, defensible decision to defer a contribution in a particular month. The problem is when it happens silently and cumulatively, and nobody tallies the gap until the reserve study comes back showing a significant funding shortfall.

A well-run board tracks the year-to-date reserve contribution as a percentage of the annual plan and discusses it explicitly. If January through June should have contributed $54,000 and the actual is $54,000, the answer is a quick "yes, we're on track" and you move on. If the actual is $44,000, you now have a $10,000 underfunding conversation that's much better to have in June than in December—or worse, in year four when the roof is failing and the fund is short.

Question 3: What Large Expenses Are Expected in the Next 60 Days That Haven't Been Approved Yet?

Every community has a pipeline of anticipated spending that hasn't formally reached the board yet. A contractor submitted a proposal for gutter cleaning that the property manager is reviewing. The annual pest control contract is up for renewal. A vendor is finishing a painting job and the final invoice—larger than the deposit—is coming.

None of these are surprises to the people managing them. But in a typical board meeting, none of them get mentioned until there's an invoice in hand and a vote needed. The result is a board that's perpetually in reactive mode: approving expenses they didn't know were coming, writing checks without a clear sense of what they're committed to spending next month.

A simple standing agenda item—"anticipated expenses in the next 60 days"—pulls this invisible pipeline into the room. The property manager or treasurer does a quick scan: anything in the queue worth flagging? It takes two minutes and changes everything. Now the board knows, before approving anything else, what's already headed toward them.

"We started doing a '60-day expense preview' at every meeting three years ago. We've never had to scramble for money since. It's not that we have more money—we just know where it's going before it arrives." — HOA Board President, Charlotte, NC

Question 4: How Do We Stand Year-to-Date Against Budget?

Budgets are not just forecasts—they're accountability tools. When the board approves an annual budget, they're making a commitment to the community about how money will be spent. Reviewing budget-versus-actual performance at every meeting keeps that commitment visible and catches drift early.

"Year-to-date against budget" doesn't need to be an exhaustive line-item review at every meeting. A summary by major category—operating expenses, administration, maintenance and repairs, reserve contributions—takes five minutes and tells the board everything they need to know about whether they're tracking to plan.

The categories worth watching most closely are usually maintenance and repairs (where unplanned work can blow a line item quickly) and administration (where professional service fees sometimes exceed estimates). A budget variance of 10 percent or more in any major category is worth a brief conversation: is this a one-time item, a systematic underestimate, or a sign of something to watch?

What you're looking for over time is the pattern, not just the snapshot. A community that routinely underspends in the spring and overspends in the fall might need to adjust budget timing, not the total. You can only see that pattern if you're reviewing actuals consistently against the plan.

Question 5: Is There Anything We're Not Talking About That We Should Be?

This question sounds soft, but it's actually the most powerful one on the list—and the hardest to get right. Every board meeting has a formal agenda, and that agenda creates a powerful filtering effect: things that aren't on the agenda don't get discussed. Information that doesn't fit neatly into a line item, a vote, or an update gets held back—sometimes indefinitely.

The property manager has noticed that a unit owner is two months behind on assessments and a third month is about to start. The treasurer saw something odd in the bank statements but it seemed minor and she didn't want to derail the meeting. A vendor sent an email suggesting that the pool pump replacement might need to happen sooner than the reserve study projected.

None of these things are crises yet. All of them are better addressed now than later. A standing question—"is there anything we're not discussing that we should be?"—creates explicit permission to surface the soft signals before they become hard problems.

The best boards use this question to cultivate a culture where nobody sits on uncomfortable information. When the treasurer knows she'll be asked every month, she comes prepared to surface the odd thing in the bank statement rather than hoping it resolves itself. When the property manager knows there's space to raise soft concerns, he doesn't wait for a formal report.